給与所得にかかる税制度

Employment Income Tax System

日本で働く外国人の給料にかかる税金は、国の税金である所得税(復興特別所得税を含む)と、地方公共団体の税金である住民税の2種類があります。所得税は税務署、住民税は区市町村が窓口になります。

Employment income of foreign employees working in Japan is subject to two kinds of taxation. One is national income tax (including the special income tax for reconstruction) and the other is inhabitant tax (local tax). Income tax is administered by Tax Offices and inhabitant tax is administered by municipal offices.

所得税

Income Tax

日本では、給与所得に対する所得税については、給与の支払者(事業主)が支払いを受ける者(労働者)に代わって所得税を徴収し、国に納める源泉徴収制度を採用しています。給与を支払う事業主には、源泉徴収が原則的に義務づけられています。さらに「居住者」と「非居住者」の区分があり、課税方法と課税範囲が異なっています。

Japan has the withholding tax system on employment income in which employers (salary payers) withhold the amount of income tax of their employees (salary recipients) from their salaries and pay the tax to the government on behalf of the employees. All employers are required to withhold and pay their employees’ income taxes levied on their salaries. The taxation methods and scope of taxable income differ depending on whether an employee is a “resident” or “non-resident.”

居住者の税金

Tax for Residents

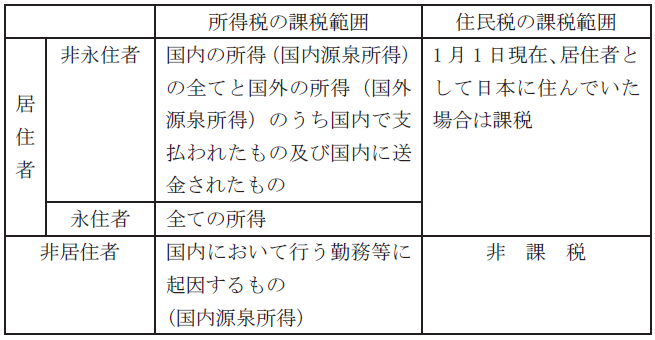

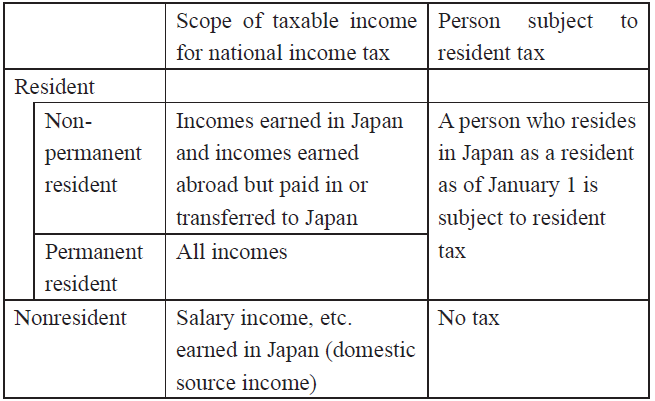

居住者と非居住者

Residents and non-residents

日本国内に「住所(生活の本拠)」を有するか、又は国内に現在まで引き続いて1年以上「居所(住所以外の現実に居住する場所)」を有する外国人は税法上「居住者」とされ、日本人と同じ税率の所得税が課税されます。ただし、給与所得者については、居住期間が1年未満であっても、労働契約等で滞在期間があらかじめ1年未満であることが明らかな場合を除いては、入国後直ちに「居住者」と推定されます。「居住者」はさらに「永住者」と「非永住者」に区分されます。「非永住者」とは、日本国籍がなく、かつ、過去10 年以内の間に日本国内に住所又は居所を有する期間の合計が5年以下である個人を指し、非永住者以外の居住者が「永住者」となります。この区分は課税範囲について違いがあり、「永住者」は原則としてすべての所得が課税対象となるのに対して、「非永住者」は国内において生じた所得(国内源泉所得)と、これ以外の所得(国外源泉所得)で日本国内において支払われたもの又は日本国内に送金されたものに対して課税されます。

A foreign national who has “domicile (core base of life )” or has had residence (place to reside other than domicile) for one year or longer in Japan, is regarded as a “resident” in terms of the tax code, and he/she is subject to income tax with the same rate as Japanese employees. However, a salary earner is regarded as a “resident” immediately after entering Japan unless his/her employment contract, etc., identifies that the period of stay is less than one year in advance. A “resident” may be either a “permanent resident” or a “nonpermanent resident.” A resident is a “nonpermanent resident” if he or she does not possess Japanese citizenship and the total period of stay in Japan during the past 10 years does not exceed 5 years. All other residents are “permanent residents.” All incomes are taxed for a “permanent resident” while only the incomes earned in Japan and incomes earned

elsewhere but paid in or transferred to Japan are taxed for a “nonpermanent resident.”

居住者の所得税額

Amount of Income Tax for Residents

居住者の所得税額の計算方法は、以下のとおりです。給与等の収入金額から給与所得控除額を控除した金額が給与所得の金額となります。所得税額は、この給与所得金額から社会保険料控除、扶養控除や基礎控除などの所得控除を差し引いて計算した金額に税率を乗じて算出します。税率は所得金額に

応じて約5%から約46%になります。なお、本国にいる家族について扶養控除を受けるためには、毎年、最初の給料支給日の前に、事業主に「扶養控除等申告書」を提出し、年末調整により、この控除を受けます。この場合、本国に送金していることを証明する書類と親族であることを証明する書類を添付することが必要です。

Amount of income tax for residents is computed as follows. Net employment income is computed by deducting employment income deduction from the amount of earnings, such as employment income, etc. Taxable income is computed by deducting social insurance premiums and income deductions such as dependent deduction or basic deduction from the net employment income. Amount of income tax is

computed by multiplying the taxable income by a tax rate ranging from about 5% to 46 %, depending on the amount of

taxable income. In addition, an employee shall submit a “Declaration about Dependents” to the employer before the first pay day of the year annually, to have a year-end adjustment made in order to get a dependents deduction for dependents residing in the home country. In this process, the employee is required to attach relevant documents to prove that he/she really sends money home, and that the recipients are indeed the employee’s relatives.

源泉徴収と年末調整

Deduction at Source and Year-end Adjustment

居住者は、毎月、事業主から給料を受ける際に、見込み税額を源泉徴収され、年末に1月から12 月までの1年間の給与総額が確定したとき、年末調整により税額が精算されます。年末調整は、事業主がその年の最後の給料を支払う際に行います。

In the case of residents, the estimated income tax amount is deducted from the monthly salary by employers, and the total amount of income tax payable is balanced through the year-end adjustment made at year’s end when the employee’s total amount of salaries for the year from January to December is confirmed. The year-end adjustment is carried out by employers upon paying the last salary of the year.

源泉徴収票

Original Record of Withholding for Employment Income

事業主は、年末調整で精算した結果を記載した「源泉徴収票」という書類を、翌年1月31 日までに、働いている人に交付しなければなりません。また、年の途中で会社を辞めた場合も、退職日から1か月以内に源泉徴収票を交付しなければなりません(所得税法第226 条)。源泉徴収票は税金を納めたことを証明するもので、確定申告をする場合にも必要ですから、必ず交付することとされています。

Employers shall issue the “original record of withholding for employment income” detailing the result of the year-end adjustment to their employees by January 31 of the following year. Employers are also required to issue the “original record of withholding for employment income” to the employees who resigned during the year within one month from the date of leaving (Article 226, Income Tax Act). The “original record of withholding for employment income” is a document which proves the tax was paid and its issuance is required for filing the final tax return.

確定申告

Final Tax Return

大部分の給与所得者の方は、給与の支払い者が行う年末調整によって所得税額が確定し、納税も完了しますから、確定申告の必要はありません。しかし、給与所得者でも次のような方は確定申告をしなければなりません。

- 給料の年間収入金額が2,000 万円を超える人

- 1か所から給与の支払いを受けている人で、給与所得及び退職所得以外の所得の合計額が20 万円を超える人

- 2か所以上から給与の支払いを受けている人のうち、給与の全部が源泉徴収の対象となる場合において、年末調整されなかった給与の収入金額と給与所得及び退職所得以外の所得との合計額が20 万円を超える人などです。詳細は税務署にお問い合わせください。

その他、申告書の提出を必要としない人でも、多額の医療費を支払ったり、住宅を取得した場合などには、申告することにより所得税が還付される場合があります。申告書は、住まいを管轄する税務署に、翌年の2月16 日から3月15 日の期間に提出します。申告の相談は税務署で受けられます。また、外国人向けのパンフレットは税務署の窓口に置いてあります。なお、居住者として所得税が課税されるべき人に対して、誤って非居住者として20.42%の税率で課税されていた場合は、確定申告では所得税の還付を受けることはできません。この場合は、事業主を通じて還付を受けることになります。

Generally, most employment income earners are not required to file a final tax return because an employer balances the amount of income tax payable at the year-end adjustment. However, the following employment income earners need to file a tax return.

- Employment income earned during the year exceeds ¥20,000,000.

- Incomes other than employment income and retirement income exceed a total of ¥200,000 for a salary earner with a single source of employment income.

- The sum of employment income for which the year-end adjustment is not made and incomes other than employment income and retirement income exceeds ¥200,000 for a salary earner from two or more sources, which are all subject to withholding taxes at source. Contact your tax office for details.

In addition, there are some cases where you are entitled to a partial or total refund of the withholding tax. You may claim a tax refund by declaring deductions for large medical expenses or special credit for the purchase of a residence, even if you are not required to file a final tax return. Tax returns need be filed between February 16 and March 15 of the following year with a tax office in the district where one’s residence is located.

An advisory service concerning filing a final return is available at the tax office. You can also get a tax leaflet in English from tax offices. However, in case a person who is supposed to be subject to income tax as a “resident” was subject to taxation as a “non-resident” at 20.42% rate by mistake, is not entitled to a tax refund by “filing a final return”. In this case, his/her employer is required to claim a refund.

外国税額控除

Credit for foreign taxes

外国人の方が本国と日本と二重に課税されることを避けるため、その年に外国で所得税にあたる税金を納めた場合、日本の所得税から「外国税額控除」を受けられる場合があります。外国税額控除を受ける場合には税務署で確定申告をする必要があります。

In order to avoid international double taxation on income, a tax payer who pays foreign taxes, national or local, which are similar to Japanese income tax may choose to have the amount of those foreign taxes credited against his/her Japanese income tax. In this case you are expected to file a final return.

非居住者の税金

非居住者については、課税範囲を限定し、国内又は国外で支払われる「国内源泉所得(日本国内での勤務に対し支払われた給料等)」が原則として課税対象になります(日本国外での勤務に対し支払われた給料等は非課税)。日本国内での勤務に対する給料等が日本国内で支払われる場合には、給与収入の金額に対して20.42%の税率で所得税の源泉徴収が行われます。日本国内での勤務に対する給料等が日本国外で支払われた場合など、所得税が源泉徴収されない場合には、その支払を受けた年の翌年の3月15 日までに税務署で確定申告し、納税する必要があります。その期限よりも前に日本を離れる場合には、離日の時までに税務署に確定申告書を提出し、納税することが必要です。非居住者については、住所を有する国と実際に居住している国による所得に対する二重課税を避けるために、日本は各国と租税条約を締結しています(アメリカ、イギリス、オーストラリア、フィリピン、韓国、中国など60 か国以上と締結)。租税条約により、特別の定めがある場合がありますので、税務署、国税局にお問い合わせください。なお、居住者として所得税が課税されるべき人に対し、誤って非居住者として課税されていた場合は、事業主を通じて税金の還付を受けることとなりますので注意してください。

住民税

Inhabitant Tax

1月1日現在、居住者として日本に住んでいた場合に住民税が課税されます。したがって、前年の所得のある人が1月1日以後に、住所を変更したり、出国しても、納税義務は消滅しないということに注意してください。住民税額は、前年の所得税の課税状況を参考にして、4月以降に各区市町村で決定され、本人に通知されます。給与所得者の場合は事業主が6月から翌年の5月まで毎月の給料から住民税額を差し引き、本人に代わって区市町村に納めます(特別徴収)。給与所得者以外の人は、本人が年4回に分けて区市町村に直接納めます(普通徴収)。住民税についても、外国税額控除や租税条約による特例が認められる場合があります。詳しくは、区市町村にお問い合わせください。

A person who resides in Japan as a resident as of January 1 is subject to residents tax. Therefore, it should be noted that the person is still subject to

inhabitant tax even if he/she changes address or leaves Japan after January 1 as long as the person had income in the previous year. The amount of inhabitant tax is decided based on the previous year’s income tax record of the person by the municipal office, and the individual is notified of the amount after April that year. If the person is an employment income earner, the employer deducts the amount of inhabitant tax from the monthly salary during the period between June that year and May of the following year, and pays it to the municipal office on behalf of the employee (special

collection). Those otherwise shall pay inhabitant tax of the previous year to the municipal office in four installments themselves (ordinary collection).

There are some cases where special measures are provided for credit for foreign taxes and the tax treaty provisions. For more details, please contact the city office in your district.

関連記事[英訳資料]登記簿謄

[英訳資料]運転免許証表面)

[英訳資料]運転免許証(裏面)

[英訳資料]役職名(役員・責任者)

[英訳資料]役職名(職種別)

[英訳資料]部門・部署名

コメント